Pleasanton Market Pulse June 2026

Market Trends

Market Trends

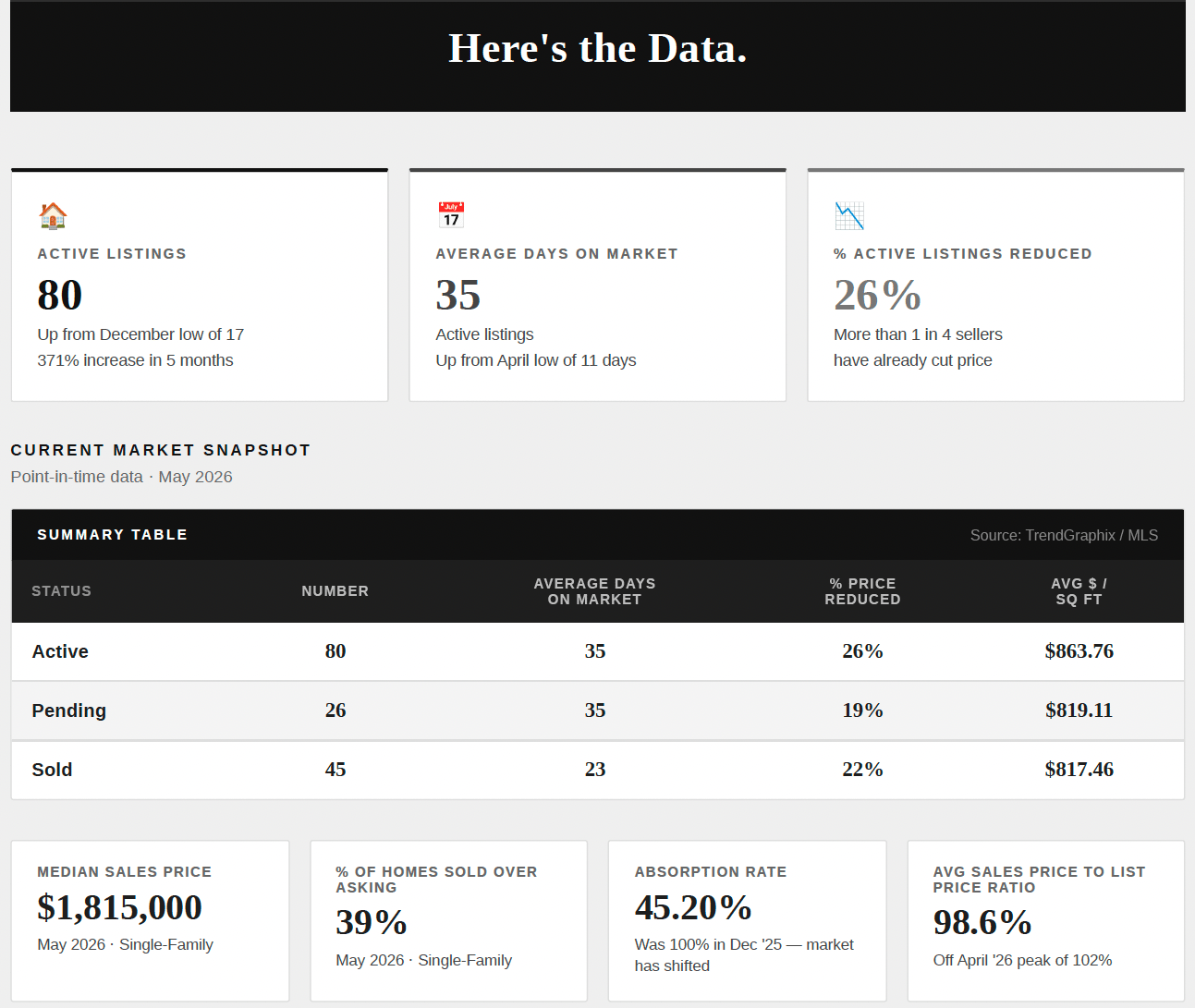

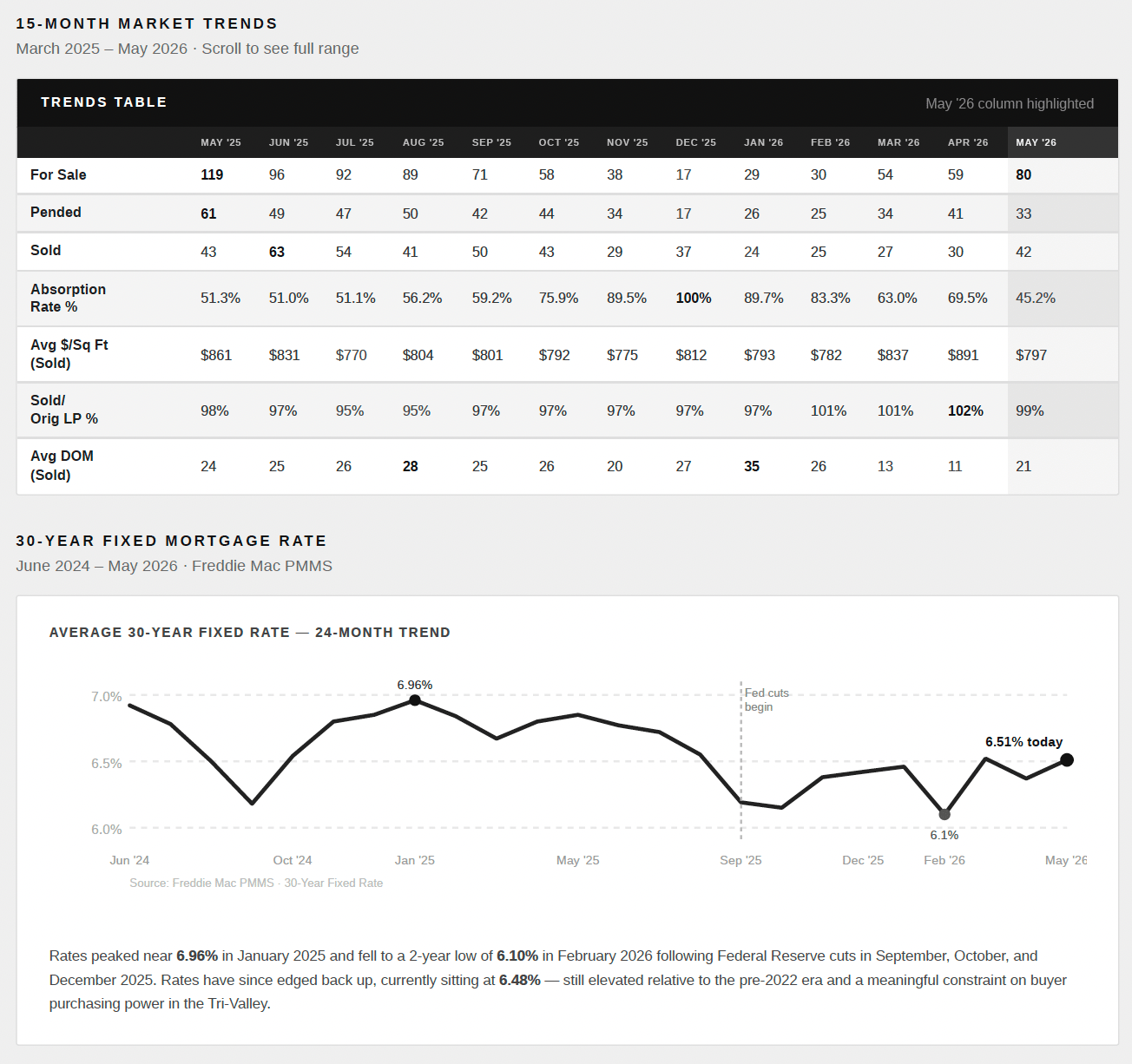

Active inventory has risen sharply — from 17 homes in December to 80 in May, a nearly five-fold increase driven by the

typical spring listing surge. Pending sales have moderated to 33 per month, and the absorption rate sits at 45.2%. For context,

May 2025 came in at 51.3% — so we're running about 6 points below last year's spring pace. That's a real decline, but not a

dramatic one. April 2025 ran even lower at 44.3%, which tells you this range isn't unprecedented for Pleasanton in the spring.

What the 15-month picture shows clearly is how much this market can move. December 2025 hit 100% absorption — every

home listed went under contract. The fall of 2025 ran consistently in the 60–90% range as inventory dried up. Today's 45.2%

reflects a spring market that has returned supply without a proportional return of demand. That gap is real, but it's also the kind

of gap that closes quickly when rates shift or inventory contracts in the fall.

Forty-two homes closed in May and 33 more went under contract. Transaction volume is healthy. With interest rates remaining

elevated, buyers' purchasing power is constrained — which hasn't killed demand so much as concentrated it. The buyers who

are active are qualified, motivated, and deliberate. They move fast on the right home and walk away from the wrong one.

Here's the number that should change how you think about this market: 39% of homes sold in May closed above their

original asking price. That's not a softening market statistic. And here's what makes it genuinely surprising — a year ago, in

May 2025, only 34.8% of homes sold over asking. The share of homes winning bidding wars has actually increased year

over year.

So why does it feel like the market has cooled? Because the other 61% tells a very different story. The average sale-to-list ratio

is 98.6%, the median sales price is $1,815,000, and 26% of active listings have already taken a price cut. This isn't a

market that's uniformly weakening — it's a market that has split in two. Correctly priced, well-presented homes are competing

harder than ever. Overpriced or underprepared homes are sitting, waiting, and eventually cutting.

This bifurcation holds at every price point. From entry-level Pleasanton to the upper end of the luxury range, some homes

move in days with multiple offers while others accumulate days on market. The difference isn't the neighborhood or the price

tier — it's the preparation and the pricing strategy.

If you're selling: The data tells you exactly what you need to do. Thirty-nine percent of homes are still closing above asking

price — yours can be one of them. But that outcome isn't automatic anymore. It goes to sellers who price to today's comps (not

April's), present the home in a way that creates genuine desire, and market it with the reach and quality it deserves. Beautiful

homes deserve beautiful marketing. The 26% sitting with price reductions didn't fail because the market failed them — they

failed to make a compelling case on day one. Don't let that be your story.

If you're buying: You have more choices and more leverage than at any point in the past year, and yet you're entering a

market where four in ten homes still attract competition. That means being selective, being prepared, and being decisive when

the right home appears. Elevated interest rates are a real constraint — but they're constraining everyone equally. Get preapproved,

know your number, and use the extra inventory to find a home that truly fits rather than settling under pressure. The

buyers winning in today's market are the ones who've done their homework.

If you're on the fence: Inventory historically peaks in late spring and contracts through fall as unsold listings come off the

market. The window of maximum choice and minimum competition is open right now. Rate relief, if it comes, will bring sidelined

buyers back quickly and shift leverage back toward sellers. Waiting for perfect conditions has a cost — and right now,

conditions are about as balanced as this market gets.

Interest rates: This is the variable with the most leverage. Rates have been the single biggest suppressor of buyer activity

over the past 18 months. Even a modest reduction — half a point — would meaningfully expand the qualified buyer pool and

shift the absorption math quickly. The Tri-Valley's high-income, tech-sector buyer base is particularly rate-sensitive at the

$1.5M–$2.5M price point. When rates move, this market moves with them.

Absorption rate through summer: At 45.2%, we're slightly below the seasonal average — not in distress, but not building

momentum either. If absorption holds or improves through June and July, the market is finding its floor and fall could tighten

meaningfully. If it slips further, expect the price reduction rate to climb past 26% as more sellers recalibrate.

New listing pace: Inventory typically peaks in May or June and contracts through fall as unsold homes are withdrawn. If listing

volume slows while pendings hold steady, the buyer advantage narrows fast — and some of today's fence-sitters will find

themselves back in a competitive environment sooner than they expect. We know the local market. We know

Stay up to date on the latest real estate trends.

Market Update

Doug Buenz | July 21, 2026

More Inventory, Selective Buyers, and Uneven Results for Sellers

Market Trends

Doug Buenz | July 21, 2026

Single-family home activity included in the MLS snapshot from June 15 through July 20, 2026

Pleasanton Neighborhoods

Doug Buenz | July 10, 2026

Compare Pleasanton's most popular neighborhoods by home prices, architectural styles, commute access, parks, recreation, and local amenities to find the community that… Read more

Neighborhood Guide

Doug Buenz | July 4, 2026

Pleasanton CA Neighborhoods: Complete Guide to Every Community (2026)

Market Trends

Doug Buenz | June 15, 2026

39% of Pleasanton Homes Sold Over Asking in May. Here's the Rest of the Story.

Market Trends

Doug Buenz | May 8, 2026

Mixed Signals Persist in the Pleasanton Market

Market Trends

Doug Buenz | April 9, 2026

Mixed Signals in the Pleasanton Market

Market Trends

Doug Buenz | December 10, 2025

Holiday Hibernation

Market Trends

Doug Buenz | October 9, 2025

A Fall Rally?