January Pleasanton Real Estate Market Update

Market Trends

Market Trends

Pleasanton real estate experienced typical market conditions in December. Inventory and pending sales both lower, and prices soft but fairly steady. The one thing that housing industry experts were hoping Santa would deliver is lower mortgage rates. But apparently Santa has little to no impact on macro-economic trends in the US economy.

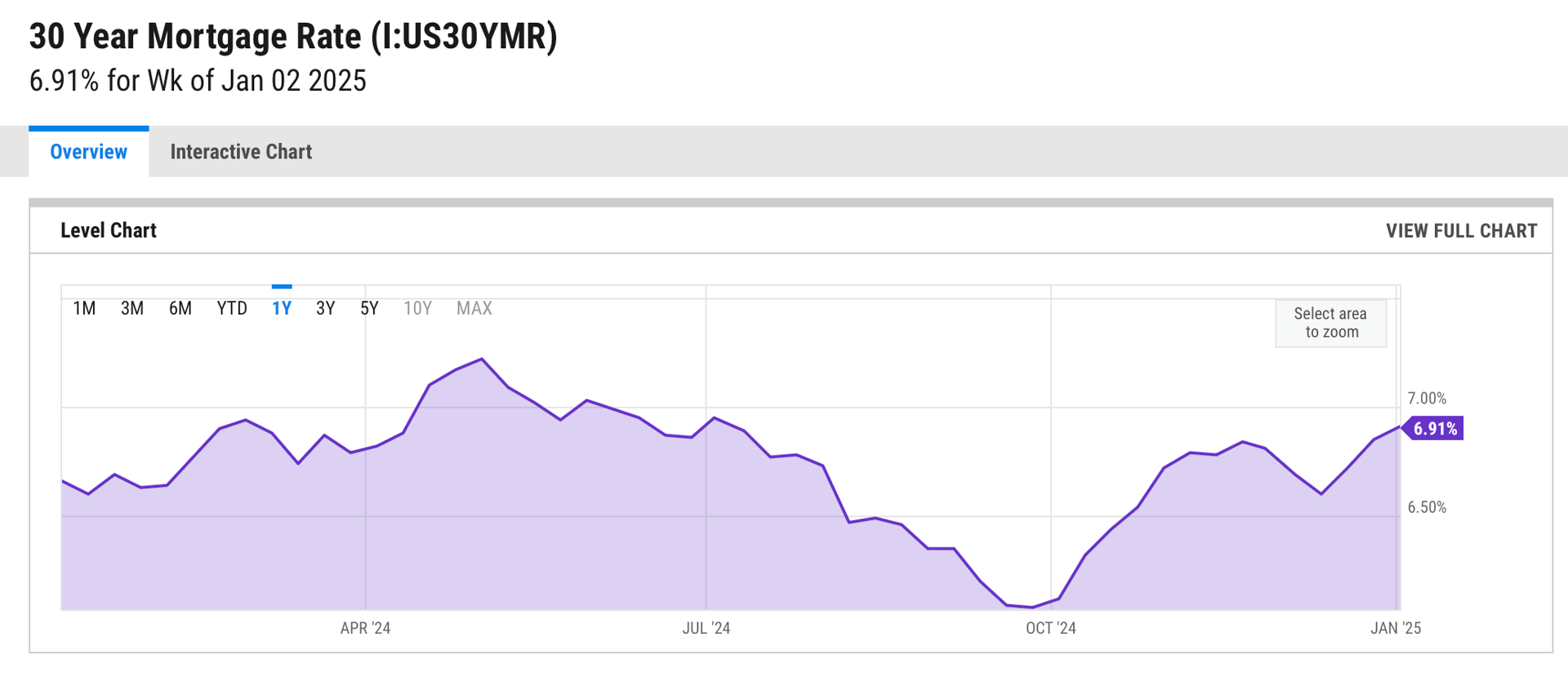

Speaking of interest rates… Average 30 year fixed mortgage rates rose again in December, to an average of 6.91%. This is up from the the 12 month low of 6.08% at the end of September of 2024, and close to the 12 month high of 7.22% in May of 2024.

This in spite of, or because of, the Federal Reserve lowering the Federal Funds Rate 3 times from 5.5% to 4.5%. In fact, if you look at the chart, mortgage rates have moved in the exact opposite direction of the federal funds rate

How can this be? The Federal Government and the Federal Reserve controls the Federal Funds Rate, the key benchmark rate that rate that impacts what banks charge for consumer and commercial short term loans. In contrast, the mortgage market is set by investors and the yield they will accept for long term loans. The inflation environment and economic outlook drives the interest rates (the yield investors are willing to accept) for long term instruments, including US treasuries and mortgage rates. Mortgage rates are market driven, not dictated by the Federal Government.

The simple explanation is that investors are fearful of inflation, which has eased in the last few months but remains above the Federal Reserve’s target of 2%. Inflation has proven to be stubborn and volatile. Trends in economic data such as jobs reports, unemployment, CPI (consumer price index), PPI (producer price index), GDP (gross domestic product), and others indicate the strength of the economy and the outlook for inflation. These are the 2 critical factors that impact the bond market, and by extension, the mortgage market.

Investors are skittish about the Fed reducing the federal funds rate if inflation is not under control, fearing that the rate reduction could heat up the economy and add to inflationary concerns. As a result, investors are demanding higher yields (interest rates) to offset expected inflation.

Simply put, mortgage rates are a critical factor in the housing market for 2025. Demand for housing has remained strong, although higher rates erode a buyer’s purchasing power and adds to uncertainty. No one expects long term mortgage rates to return to the artificially low 3% range of the pandemic. But a return to historically normal rates in the 5% range would certainly help the housing market. As always we will see…

Stay up to date on the latest real estate trends.

Market Update

Doug Buenz | August 7, 2026

August 2026 Update: Well-positioned homes sold quickly and averaged 102% of asking, while homes taking over 30 days averaged just 94%.

Pleasanton Real Estate

Doug Buenz | July 28, 2026

The most common reasons Pleasanton homes fail to attract offers—and what sellers should consider before relisting.

Market Update

Doug Buenz | July 21, 2026

More Inventory, Selective Buyers, and Uneven Results for Sellers

Market Trends

Doug Buenz | July 21, 2026

Single-family home activity included in the MLS snapshot from June 15 through July 20, 2026

Pleasanton Neighborhoods

Doug Buenz | July 10, 2026

Compare Pleasanton's most popular neighborhoods by home prices, architectural styles, commute access, parks, recreation, and local amenities to find the community that… Read more

Neighborhood Guide

Doug Buenz | July 4, 2026

Pleasanton CA Neighborhoods: Complete Guide to Every Community (2026)

Market Trends

Doug Buenz | June 15, 2026

39% of Pleasanton Homes Sold Over Asking in May. Here's the Rest of the Story.

Market Trends

Doug Buenz | May 8, 2026

Mixed Signals Persist in the Pleasanton Market

Market Trends

Doug Buenz | April 9, 2026

Mixed Signals in the Pleasanton Market