Mortgage Rate Primer

Tips & Advice

Tips & Advice

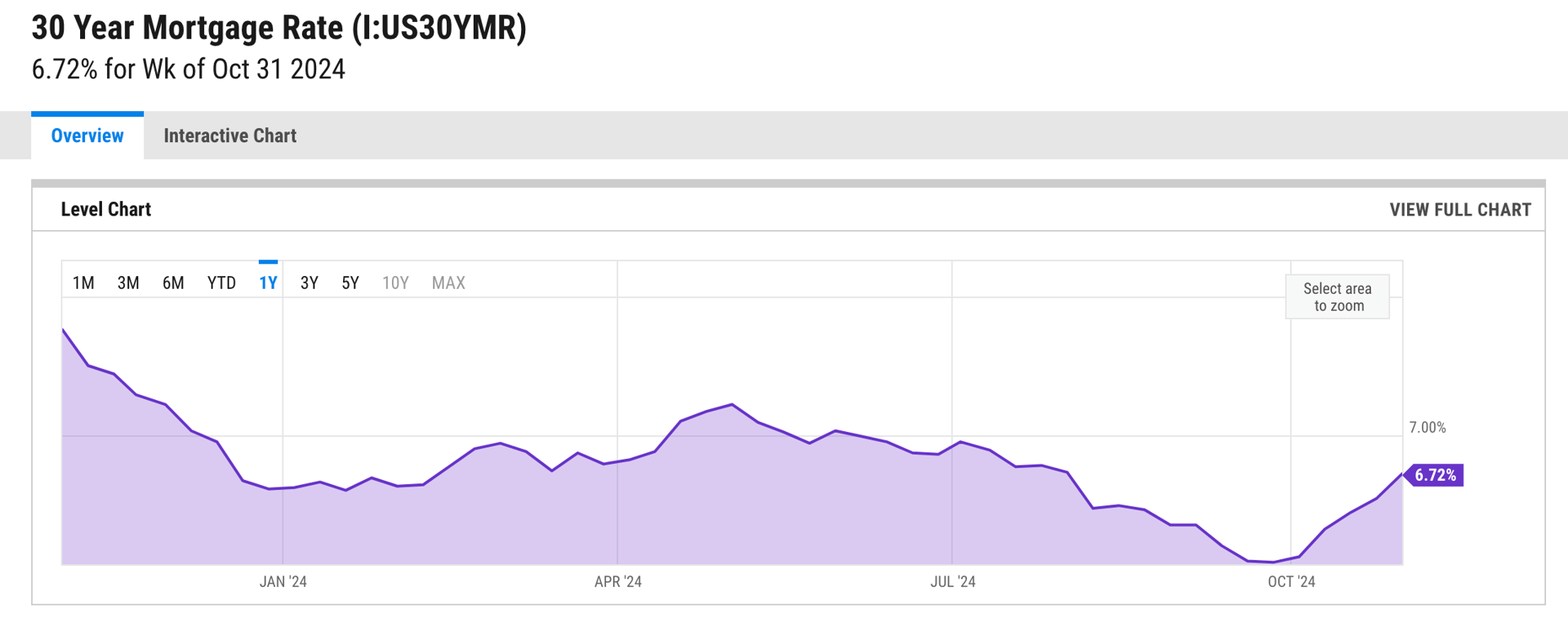

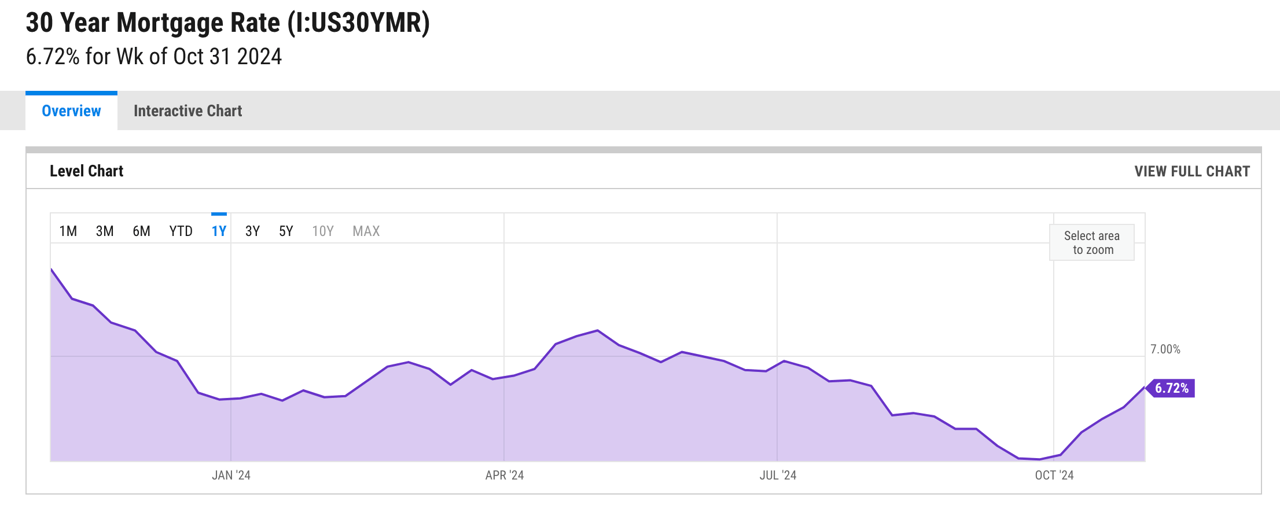

One of comments I hear a lot from the public is “The Fed lowered mortgage rates so the market should be better”. At the risk of wading into economics, a subject most people find about as interesting as watching paint dry, it is important to clarify how mortgage rates work.

Simply put… the Federal Government does not control mortgage rates. However, the Federal Reserve (“the Fed”) does set the Federal Funds Rate, which is a bell weather rate that banks charge to lend funds to other banks on an overnight basis. This interest rate influences short term rates such as the prime rate, as well as consumer loans and credit cards. More importantly, it signals the Fed’s outlook on the economy and inflation, and impacts the broader investment environment.

The Fed acts as the driver of the economy, using monetary policy as a gas pedal or break depending on conditions. They accomplish this by lowering or raising the Federal Funds rate. When the economy is slowing, the fed can lower the Federal Funds rate to stimulate the economy. When the economy is too robust or inflation is higher than their target, they can raise the Federal Funds rate to slow economic growth and (hopefully) tame inflation.

The mortgage market is not controlled by the Fed, but rather is essentially a bond market driven by investors and the rate of return (interest rate) they are willing to accept when taking into account inflation and the long-term economic outlook. Mortgage rates most closely track the 10 year Treasury market. As we have seen, even though the Fed recently lowered the Federal Funds Rate, average mortgage rates have risen by about .75% since the beginning of October. How can this be?

One word… inflation. The answer is investors are simply not convinced inflation will hit the Fed’s target rate of 2%, so they will demand a higher rate of return to offset the effects of higher inflation. If investors think that lowering the Federal Funds Rate will fuel more inflation, they will demand higher returns in the form of higher interest rates.

Stay up to date on the latest real estate trends.

Pleasanton Real Estate

Doug Buenz | July 28, 2026

The most common reasons Pleasanton homes fail to attract offers—and what sellers should consider before relisting.

Market Update

Doug Buenz | July 21, 2026

More Inventory, Selective Buyers, and Uneven Results for Sellers

Market Trends

Doug Buenz | July 21, 2026

Single-family home activity included in the MLS snapshot from June 15 through July 20, 2026

Pleasanton Neighborhoods

Doug Buenz | July 10, 2026

Compare Pleasanton's most popular neighborhoods by home prices, architectural styles, commute access, parks, recreation, and local amenities to find the community that… Read more

Neighborhood Guide

Doug Buenz | July 4, 2026

Pleasanton CA Neighborhoods: Complete Guide to Every Community (2026)

Market Trends

Doug Buenz | June 15, 2026

39% of Pleasanton Homes Sold Over Asking in May. Here's the Rest of the Story.

Market Trends

Doug Buenz | May 8, 2026

Mixed Signals Persist in the Pleasanton Market

Market Trends

Doug Buenz | April 9, 2026

Mixed Signals in the Pleasanton Market

Market Trends

Doug Buenz | December 10, 2025

Holiday Hibernation