Our Inside Real Estate topic is Property Taxes in California. If you buy a home in California, especially if you are from out of state, California taxes can be a little bit different than the rest of the country.

Here is how they work: basically, the property is assessed by the tax assessor at the market value at the time you purchase the property. Normally, that is the price you would pay if you get an extremely good buy, the assessor could theoretically challenge that value and claim a higher value for market value. But for all intents and purposes, the price you pay is the assessed value of the property.

That assessed value can only increase by 2% a year. Therefore, your property tax payments can only increase by 2% a year. That is a result of Prop 13, which was passed in the 1970’s to put a limit on property tax increases.

The rule of thumb is, property taxes will run you about 1.2% of the assessed value. It could be a little bit lower for older homes or if you are in the county and it can be a little bit higher for some of the newer homes. But 1.2% is a pretty good rule of thumb for what your property taxes will be. Of course, that is 1.2% of the assessed value and that goes up 2% a year.

Out of the 1.2%, the county gets 1%. The 0.2% is basically a compilation of additional assessments that are charged by the city and the municipalities and the states and they are often bond measures that cover things like BART, local schools, flood control, mosquito abatement, East Bay Open Space, et cetera. All of that added together typically comes in about 1.2%

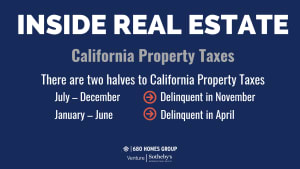

Property taxes are collected in two halves and they are split. It is usually a 2018/2019-tax year and a 2019/2020-tax year. The first half of the property tax bill covers July through the end of December. Those taxes are due October 10th and delinquent November 10th. The second half of the property tax year covers January through June. Those taxes are due on March 10th and delinquent April 10th. That is when the tax payments are due and what they cover.

Sometimes we get questions about Mello-Roos. What is Mello-Roos? It is simply a mechanism for newer home developments to finance all the infrastructure, streets, streetlights, et cetera using bonds that are attached to the property tax payment. If you buy a home in a newer development that has Mello-Roos assessments, that property tax rate can go up as high as 1.6 or even 1.8% of the value. If you are buying a new home or you are buying a home that is relatively new, you want to check that property tax assessment to make sure that you understand what your obligations going to be.

If you have any other topics you would like to see us address in future episodes, please let us know in the comments. If we can help you or anyone you know with their real estate needs, please do give us a call at 925-785-7777 or visit us at

680homes.com